MPI 2024 Manufacturing Study: Key Takeaways

The MPI 2025 Manufacturing Study launches this quarter, so we are publishing select data from our 2024 study, which was previously available only to MPI paid clients. MPI has been conducting the in-depth study since 2003. This article describes four key findings from the 2024 study.

Productivity rises despite persistent challenges and a preference for the status quo

The 2024 MPI Manufacturing Study of 413 global plants found new insights into workforce and cost challenges that have persisted for more than decade. But the Study also found rising productivity — and a positive outlook for capital investments.

Labor challenges linger even as wages rise

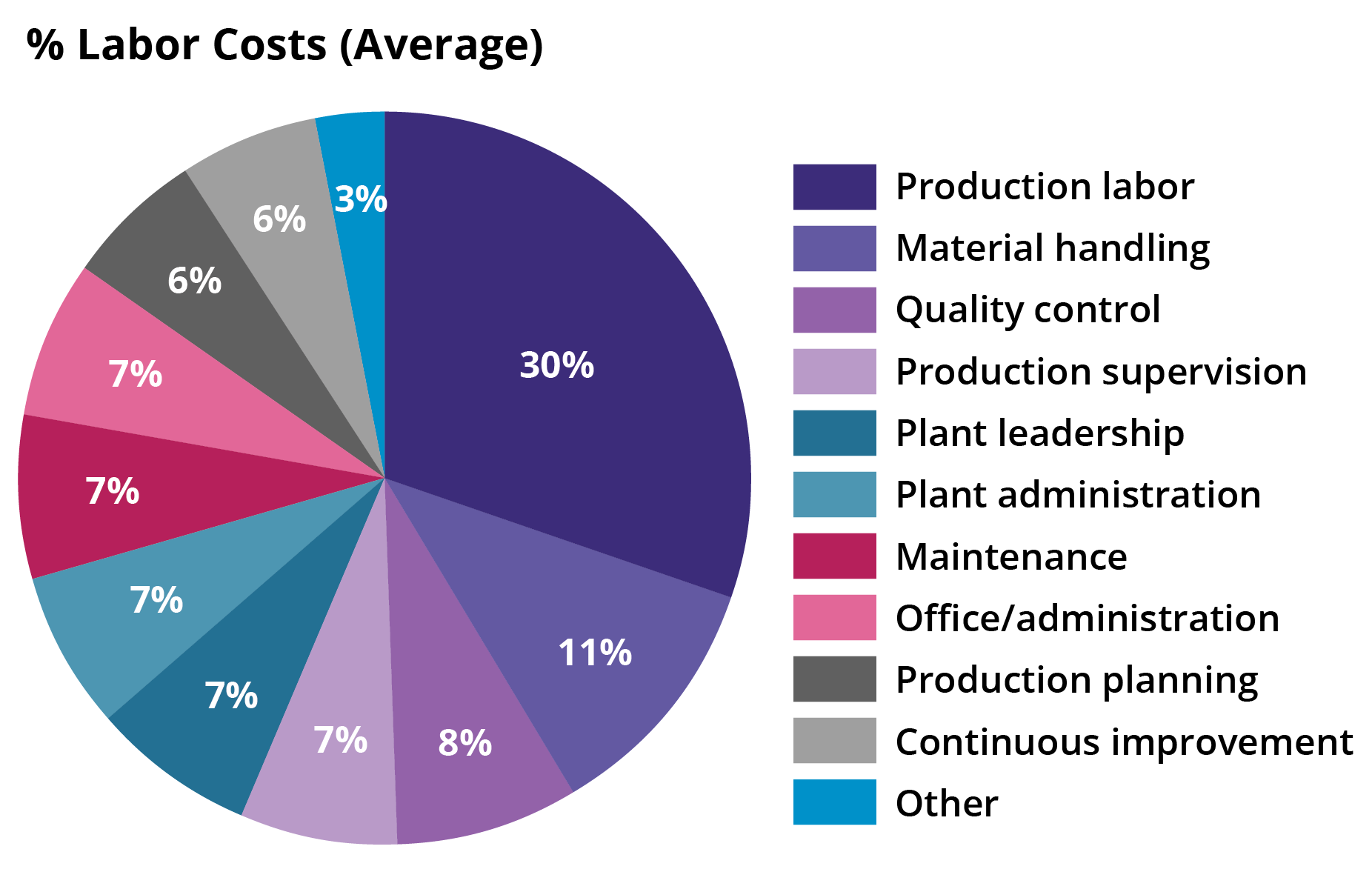

The 2024 MPI study explored — for the first time — labor costs by activity. Production labor was by far the largest component of labor costs for manufacturers at 30% — nearly 3X the second-highest category (material handling). Work that involves touching the product — production labor, material handling, and quality control — comprised half of all labor costs for manufacturers (Figure 1).

Figure 1. Percentage of labor costs

This finding emphasizes the impact of workforce challenges plaguing manufacturers for the last decade, most notably finding and keeping employees. For example, despite a jump in average hourly starting wages from $13 in 2014 to $22 in 2024 for production employees, 68% of manufacturers said it was somewhat difficult, very difficult or impossible to fill frontline production roles. This challenge affects other key roles as well (Figure 2).

Figure 2. Percentage who said role is difficult or impossible to fill

Average labor turnover (36%) and absenteeism rates (30%) also remained high, another reflection of long-term labor challenges.

Fortunately, manufacturers are investing more in training — an average of 19% of revenues in 2024 vs. just 12% in 2021. Since the 2018 Study, more than 50% of manufacturers have offered more than 20 hours a year in training.

Inflation amplifies and widens cost pressure

The study results reflected the widespread influence of inflation in 2023 and 2024. Most manufacturers reported that all costs increased over the previous 12 months, including:

- 80% reporting increased utility/fuel costs, and

- 75% paying more for logistics/transportation, employee wages, and components/materials.

Not surprisingly, 73% of manufacturers raised their own prices.

Rising costs were reflected in the total cost of goods sold (COGS) as a percentage of plant sales, rising from 60% in the 2020 Study to 67% in 2024. And nearly a quarter of manufacturers reported that per-unit manufacturing costs — excluding materials — increased by more than 10% over the previous three years.

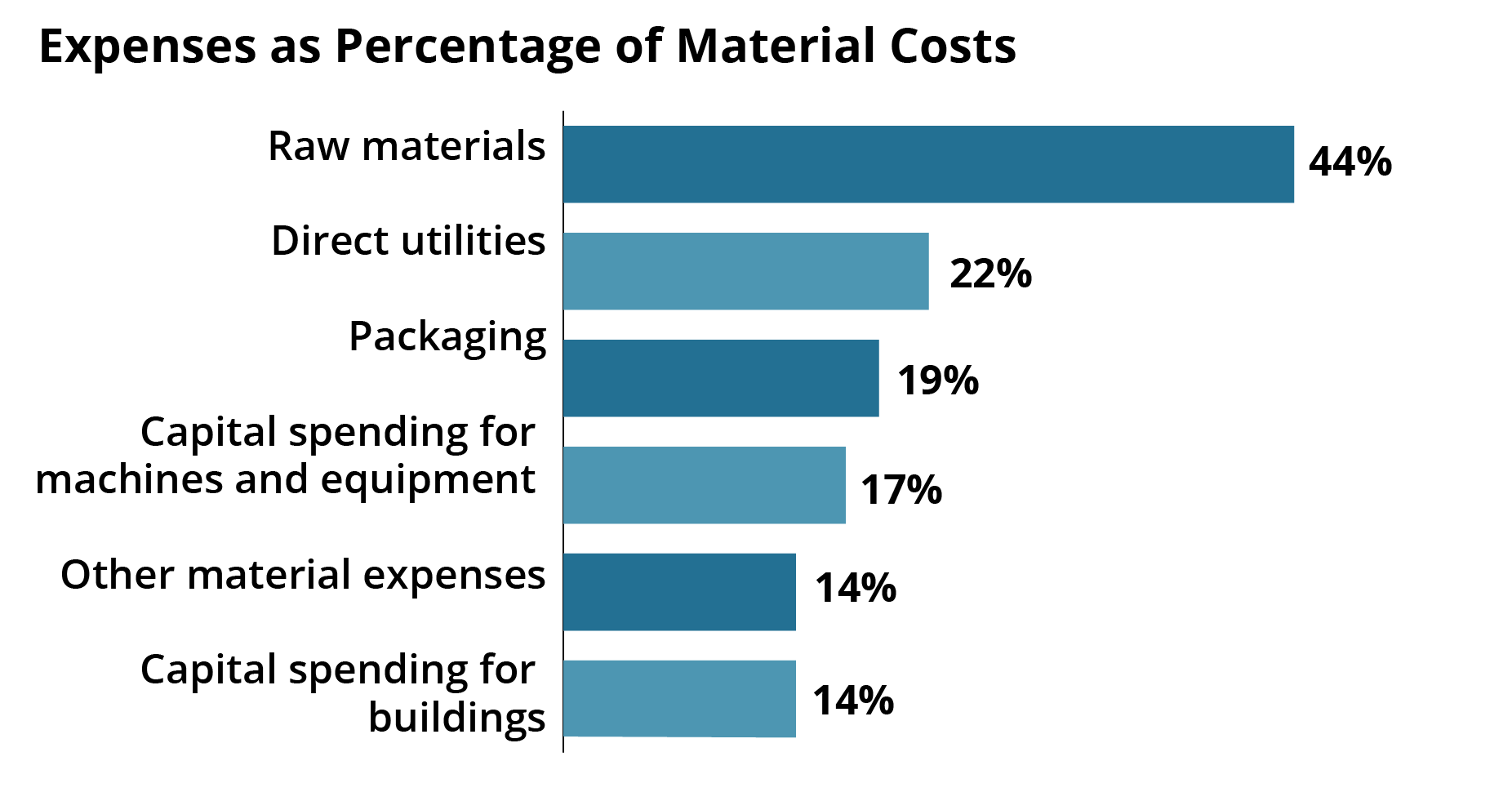

A new question in the 2024 Study delved deeper into material costs. Raw materials, energy, and packaging were the top three expense categories (Figure 3).

Figure 3. Expenses as percentage of material costs

Higher productivity, but more transactional relationships

Despite ongoing labor challenges, rising expenses, and lingering disruptions from the global pandemic, manufacturers have become more productive. Average production volumes as a percentage of capacity rebounded from 62% in the 2020 Study to 69% in 2024, and productivity increased for 72% of manufacturers over the previous three years.

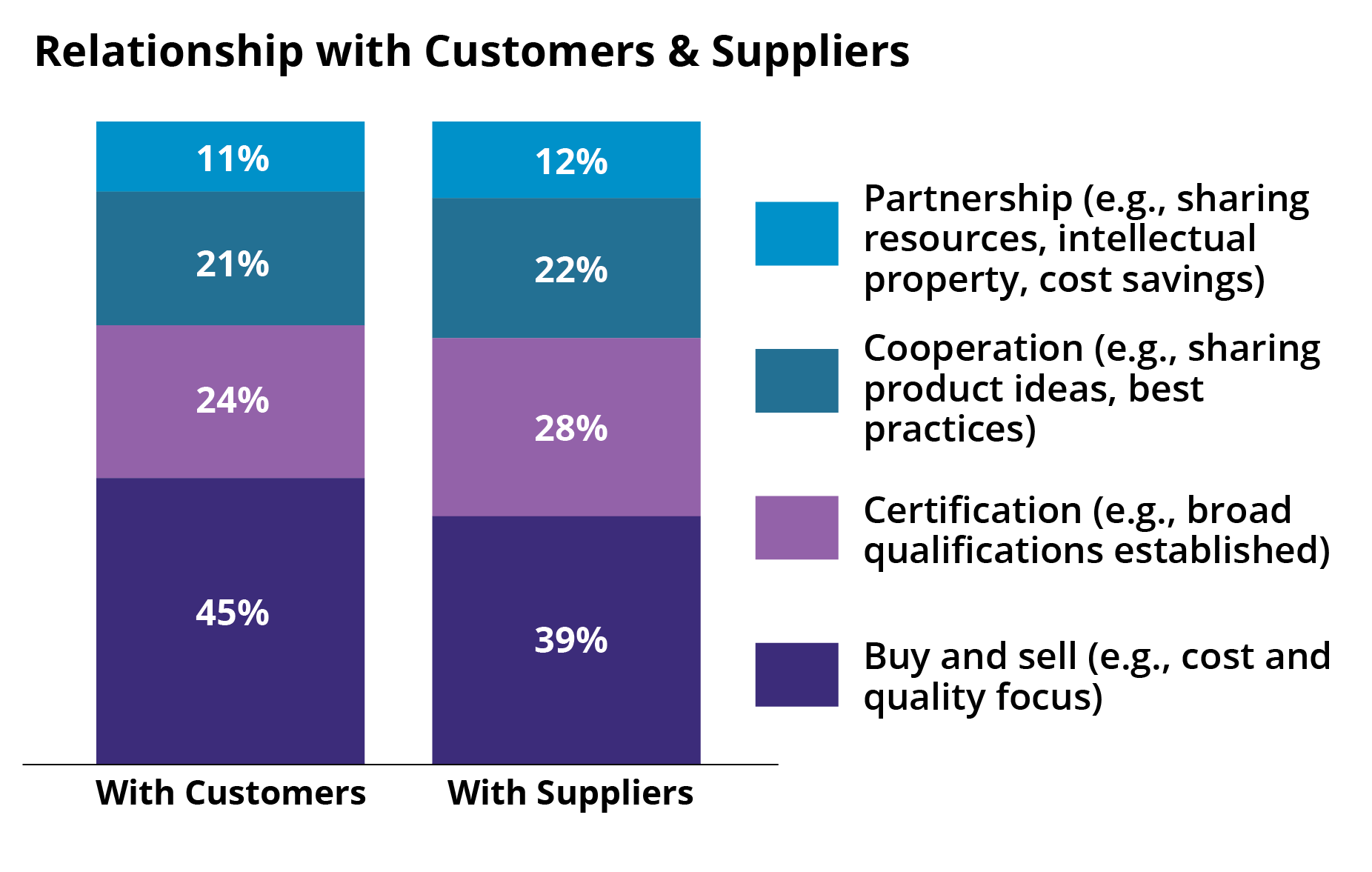

However, many manufacturers still appeared to be stuck in “pandemic mode,” prioritizing short-term gains over practices that generate long-term value, such as collaborative supplier-management practices. In fact, relations with both suppliers and customers were still “buy and sell” for a high percentage of manufacturers (Figure 4).

Figure 4. Relationship with customers and suppliers

Despite unhappy memories of supply-chain delays and limited material and component availability, inventory practices have not changed significantly. Manufacturers were managing inventories in 2024 in roughly the same ways they did in 2020:

- Raw material: average 35 days in 2024 vs. 31 days

- Work-in-process: average 28 days vs. 26 days

- Finished goods: average 26 days vs. 29 days

Digital technologies and machine failures will drive investment

Spending on IT investments — hardware and software — and capital equipment were likely to increase for a large majority of manufacturers. Two-thirds planned to increase capital equipment spending during the coming year; 69% expected to increase spending for hardware, and 70% expected to increase spending on software.

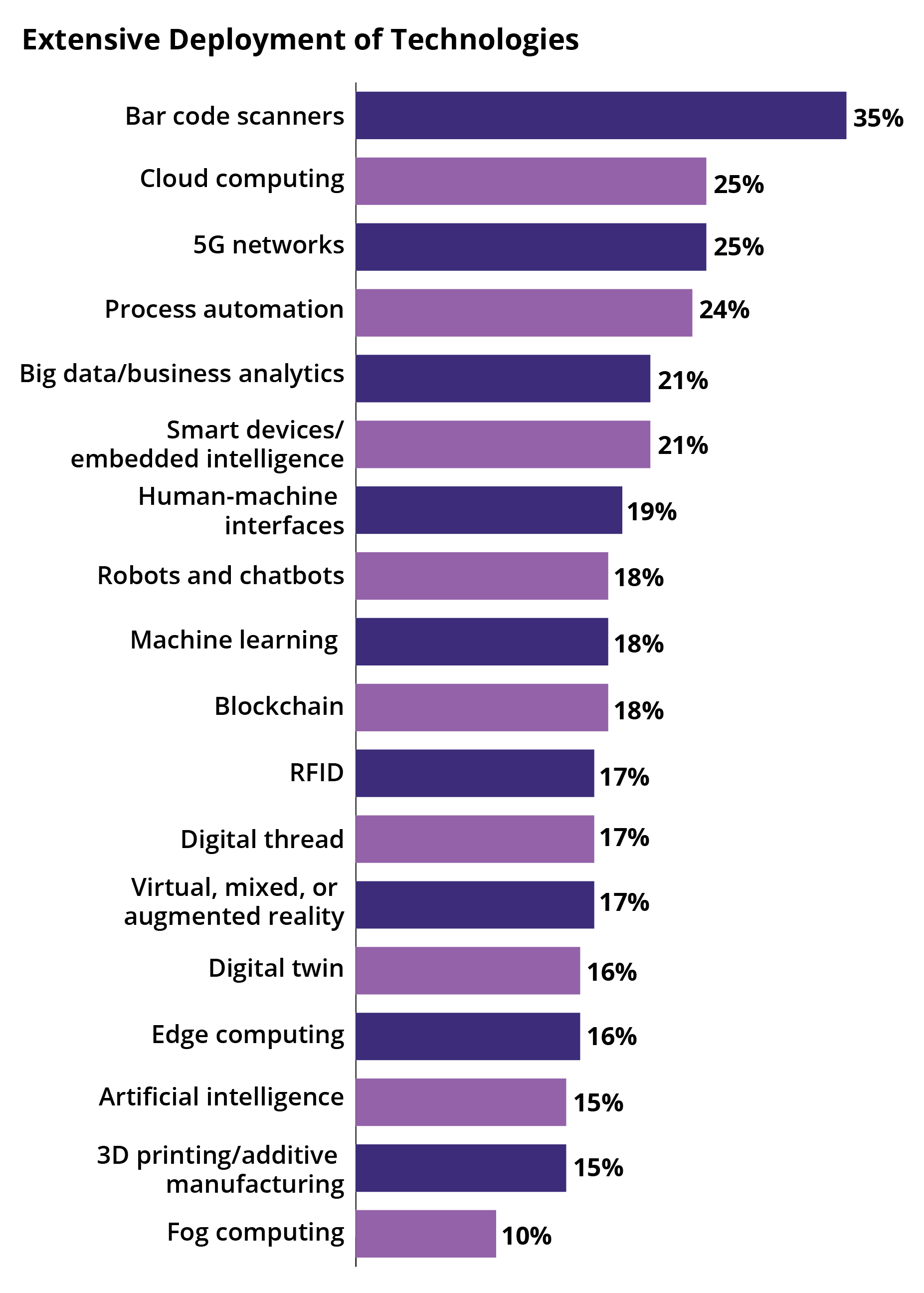

A trend that driving investment is continued deployment of digital technologies. Data from the 2024 Study shows that relatively few plants reported extensive deployment of beneficial technologies (Figure 5), so there are broad opportunities for improving operations through adoption.

Figure 5. Extensive deployment of technologies

Another trend likely to drive increased investment in capital equipment is machine wear and tear. The 2024 Study found that more than a third (35% average) of machine maintenance jobs are reactive. And 37% of plants report an average mean time between failures for equipment of 24 hours or less.

How to access and apply more study findings These takeaways are a fraction of the data available from the MPI Manufacturing Study. Also included are additional measures and practices for:

- Workforce performance

- Production performance

- Customer and supplier performance

- Maintenance performance

- Green performance

Looking for more insights into the data and the ability to compare findings specific to your operations or the operations of your clients?

The MPI Benchmarking Toolkit now includes all the 2024 study findings, and allows users to sort the data by:

- Industry

- Plant profile characteristics (volume and mix, plant revenue, country/region, etc.)

- Study years

Schedule an appointment with John Brandt, MPI CEO, to learn more.